The $102 billion food and grocery sector is a tough market. Just ask Coles, who reported a third quarter sales increase of just 1.9 per cent in late April. Woolworths reported slightly better at 4.9 per cent.

The $102 billion food and grocery sector is a tough market. Just ask Coles, who reported a third quarter sales increase of just 1.9 per cent in late April. Woolworths reported slightly better at 4.9 per cent.

The entry of German discounter Aldi and a decade of ‘price wars’ has produced a price-conscious consumer, who regularly switches between supermarket brands seeking the lowest price.

As Kaufland gears up for its entry into the Australian market, the one thing we can be sure of is that things are going to get tougher for incumbent players.

A new direction

Eyebrows must have been raised back in 2016, when department David Jones signalled they planned to enter the crowded food market. A tactical error, or an astute decision? Ultimately, DJs CEO John Dixon and Food MD Pieter de Wet have identified a gap in the Australian grocery market and are preparing to exploit it with their David Jones Food Halls; with a respectful nod to the iconic Marks & Spencers food halls in the UK.

Dixon and de Wet have got skin in the game. Dixon, joined David Jones from UK retailer Marks & Spencer and de Wet, with over a decade in food and grocery leadership with Woolworths South Africa, stepped in as group executive of food, before being appointed to the more senior role of managing director, reflecting the importance of food in David Jones’ growth strategy.

Markets within markets

Like the UK and Europe, the Australian grocery market has split into discounters at one end and mainstream supermarkets at the other. While the growth of discounter-style grocers continues to outperform supermarkets globally, the premium market in Australia appears ripe for exploitation and signals the ever-changing face of the Australian food and grocery landscape.

Globalisation, innovation, multiculturalism, media, travel and the internet have shifted the power from the retailer to the consumer. Information-rich food shoppers are now more empowered to make decisions than ever before. Reality television cooking shows and gourmet food markets tempt shoppers to seek out exclusive, unique food experiences. The days of ‘meat and three veg’ have long gone.

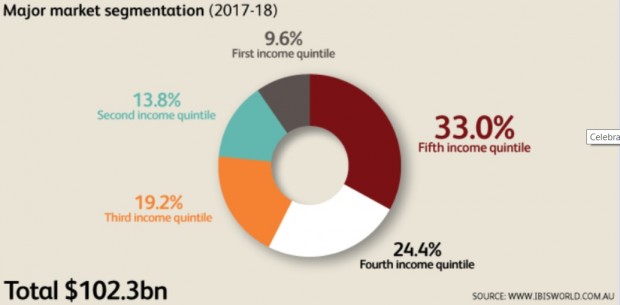

Retailers develop brands to meet demand from consumer segments. If the segment is viable, ultimately the brand succeeds. IBISWorld has examined key consumer segments, referred to as quintiles, who purchase food and groceries. Analysis is based on the revenue derived from these major consumer segments as a percentage of total supermarket industry revenue – which accordingly provides an indication of the size of each market.

Consumers in the first and second income quintile spend the highest proportion of their reasonably low income on food and groceries, and represent nearly 24 per cent of the revenue to the sector.

This segment of shoppers are attracted to lower-priced private label products and have become regular Aldi shoppers.

The third quintile of household income earners consists of low-to-medium income families and represents 19 per cent on industry revenues.

This group is likely to purchase a range of both private-label and branded products, and often attracted to weekly specials and deep discounting. The fourth income quintile, representing over 24 per cent of industry revenue, is in growth and comprises larger families and busy time-poor professionals. This group seeks convenience, click and collect transactions, ready-made meals and meal solutions.

The final quintile currently contributes over a third of supermarket revenues and represents the highest 20.0 per cent of household incomes. While this consumer allocates the lowest percentage of their sizable income on groceries, they spend the greatest amount in absolute terms.

Supermarkets have increasingly expanded the range of premium products in-store to boost demand from this market. It is this market that David Jones is chasing.

Value is not just about low price

While price has certainly been the driver of Australian supermarket growth and market share over the past decade, in recent months we have seen both major supermarkets subtly move away from focusing on this attribute to an emphasis on other important aspects of their offer; such as freshness, range, quality, service and convenience.

While no one expects to see food pricing move upwards dramatically, prices will plateau and become stable. As such, consumers will seek more value for their money.

Without deep discounting, consumers will look to supermarkets that offer more for their hard-earned dollars – in terms of value, convenience, quality and range.

Globally, supermarkets that have leveraged a premium strategy selectively, have found it successful in cushioning the effects of competitors’ increased price discounting activity.

Offering juice bars, free wine tasting, premium products and local food, are all elements that feature in UK supermarket Waitrose’s bid to continue to grow in a grocery market increasingly driven by discounters like Aldi and Lidl.

Similarly, US supermarket Whole Foods had repositioned itself as the “healthiest grocery store” before being snapped up by Amazon in August 2017. In Australia, NSW grocer Harris Farms has positioned themselves with ethical consumption attributes, like sustainability, supporting communities and farmers. Frewville’s Foodland in Adelaide continues to win international awards, not on price but on building strong partnerships, unwavering quality, integrity and shared values.

Great strategy or risky move?

Entry into the food and grocery sector without careful planning is a risk for David Jones given the current competitive nature of the sector. However, it looks like they have the right team and expertise to pull this off. The biggest issue David Jones will face is the lack of an extensive supplier base.

Unlike their general merchandise and apparel categories that source inventory overseas and import into a country, food retailers are highly dependent on domestic supply.

Previous attempts to launch an upmarket grocer in Australia have failed. Jones the Grocer’s Australian operations went bust in December 2014. Woolworths finally pulled the pin on their Thomas Dux Grocers in mid-2017. It is therefore reasonable to think that if Australia’s biggest food and grocery retailer, Woolworths, could not make it work, how can David Jones?

Certainly one of the challenges Woolworths faced with their Thomas Dux venture was the costs incurred in ‘stand-alone’ sites, despite having premium locations in upmarket suburbs. Revenues were simply not viable to support a stand-alone business.

While David Jones has hinted at potentially opening a stand-alone version, their immediate strategy will be to open food halls in existing stores.

A smart move, considering traditional departments store categories like apparel, bedding and consumer electronics, have been severely impacted by global fast fashion retailers and category killers, like Harvey Norman and JB Hi-Fi.

They have available space, existing leases and such a move will allow them to reduce the footprint of loss-making categories.

Clearly, targeting shoppers seeking premium, exclusive food products will represent a very small but profitable segment – if well executed. Careful selection of store locations and securing supplier support could drive long-term growth for Woolworths SA. Following a Marks & Spencer model, possibly co-located food stores within David Jones department stores, may be the safest way to enter the market.

Food remains a dynamic sector

It is evident that Australia is becoming an attractive market for international food and grocery retailers, with its growing middle class, multicultural tastes and relatively strong economy. Global players such as Aldi and Costco have already set up shop and continue to expand. Kaufland is about to launch and rumours still surround whether Lidl will follow, after Kaufland establishes itself within the market.

As the food and grocery segment continues to offer up new segments, new players will continue to enter, bringing with them greater choice for consumers and stronger bargaining power for suppliers.

Dr Gary Mortimer is associate professor in marketing and international business at QUT Business School.