The expansion of major global brands such as H&M and Zara into the homewares category poses a challenge to established local retailers, with new data released by IbisWorld forecasting double digital growth in the sector over the next five years.

According to IbisWorld senior industry analyst, Lauren Magner, if the market penetration of fast fashion companies’ homeware and furniture ranges matches that of their fashion ranges, double digit growth in homewares is anticipated over the next five years.

“Companies operating mainly in the Australian market will suffer due to a lack of scale, particularly in design and procurement, and the fact that they are often slower to bring on-trend items to market,” said Magner.

Fast fashion in the home

Zara confirmed in Janauary it would open its first Zara Home store in Australia this month at Highpoint Shopping Centre in Victoria, followed by a second store at Pitt St Mall in Sydney later this year.

According to Ibisworld, relatively high disposable incomes tend to make Australia a natural target for lifestyle companies. Increasingly, major European and US players are expanding into Asia to pursue growth avenues.

Brands such as Zara and H&M have quickly developed a dedicated following in Australia, and these companies are expected to leverage their reputations to attract consumers to their affordable homeware ranges.

Lower pricepoints and existing expertise in the sourcing of fabrics have offered fast fashion retailers an advantage in the homewares market when producing soft furnishings such as cushions, throws, and rugs.

“One of the advantages for brands like Zara Home is that they are not destination retailers like Ikea or Harvey Norman, which customers will often visit on a weekend or planned outing. Zara will benefit from people visiting and browsing during their lunch break, or while looking at fashion, and making impulse homeware purchases,” said Magner.

The future for furniture

Beyond homewares, there have also been new furniture entrants to the market, seeking growth avenues outside of the traditional markets of North America and Europe. Unlike fast fashion homewares retailers, these stores emphasise quality, appealing to sophisticated consumers that appreciate the broader range of products offered overseas.

Players in the furniture market are able to provide a wide range of products through a relatively small number of stores, due to their scale and access to overseas manufacturing and distribution channels.

“Alongside the fast fashion players, some high end international companies like Pottery Barn and Ashley Furniture are also expanding their brand outside the mature American market,” added Magner.

Ongoing expansion in clothing

Fast fashion is expected to continue to expand into local retail markets in 2015. The clothing and accessories retail sector is forecast to earn $20.9 billion in revenue in 2014-15, however, as it is a mature and relatively saturated sector, revenue has declined at a compound annual rate of 1.2 per cent over the past five years.

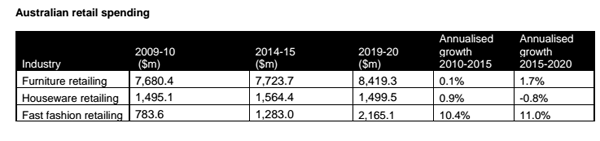

Fast fashion is one of the few categories within the clothing and accessories sector that is exhibiting growth, with compound annual growth of 10.4 per cent over the past five years.

“This indicates that fast fashion retailers are attracting consumers’ attention at the expense of other forms of retail,” said Magner.

Since it began operating in Australia, Zara has averaged a strong operating margin of almost 25 per cent – which is higher than that of the broader Australian clothing, footwear and personal accessory retailing sector – primarily due to their product innovation and strategic store fitouts.

H&M, Sephora, Uniqlo, Victoria’s Secret, Topshop, and luxury US brands such as Michael Kors and Coach are also expected to expand their presence in Australian retailing in 2015.