When you think of retail franchising, it is most likely global franchisors McDonald’s, KFC, or Subway will be among the first brands that come to mind.

When you think of retail franchising, it is most likely global franchisors McDonald’s, KFC, or Subway will be among the first brands that come to mind.

Each of has a strong presence in Australia, but the biggest franchisor in this country is a grocery and liquor wholesaler that has morphed into a franchisor.

The IGA supermarket banner, owned by Metcash, is the largest franchise brand in the country in terms of its store network and sales.

The three tier IGA supermarket network has 1393 stores, just ahead of Subway with 1377 franchise outlets in Australia, the retailer’s biggest market outside the US where it started in 1965.

Subway, which launched in Australia with a store in Perth in 1988, has added more than 100 stores in Australia in the past two years.

The IGA store network has also been growing in the past two years, boosted by the acquisition and conversion of the Franklins supermarket chain.

IGA is also an ‘imported’ brand from the US, established there in 1926 by 100 retailers from New York and Connecticut.

Metcash introduced the IGA brand to Australia in the 1990s as part of a banner rationalisation program by CEO, Andrew Reitzer.

The launch of IGA effectively re-engineered Metcash from a wholesaler to a franchisor, confirming a profound shift from simply providing goods to retailer-controlled banners to supplying retailers tied to a brand owned and controlled by Metcash.

Reitzer came to Australia from South Africa in 1998 to run the Davids grocery and liquor wholesaling business, which was acquired by South Africa’s Metro Cash & Carry.

Davids was struggling with its customer base, trading under various different brands, and losing market share to the major chains, Woolworths and Coles.

Reitzer could have adopted one of the bigger local brands or introduced an entirely new brand as part of his strategy to merge the various banners to create a stronger and more coherent independent brand in the market.

He chose IGA because it provided Metcash with systems, disciplines, and marketing concepts to assist in lifting the presentation, service standards, and trading performance of the independent supermarkets.

Since 1998, Reitzer has transformed the former grocery and liquor wholesaler, acquiring Perth-based wholesaler, Foodland Associated, and the Franklins retail chain, which have been rebadged to IGA and on-sold to independent retailers.

He has also ventured further afield, acquiring the Mitre 10 hardware chain and the Autobarn and Autpro automotive accessories brands.

Listed on the Australian Stock Exchange, Metcash has eight retail brands in the Inside Retail Magazine Top 50 Franchises list, ranked by the number of outlets in their store network.

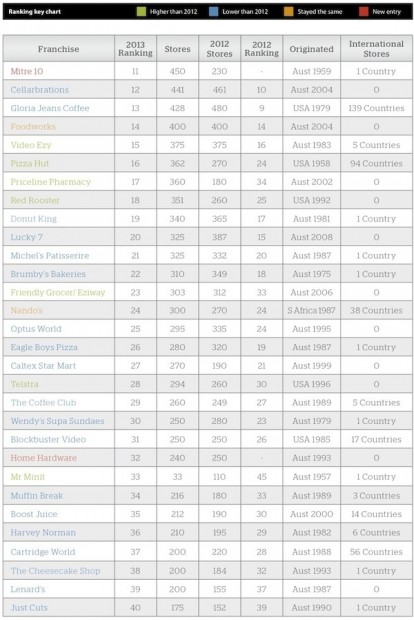

The Metcash brands are IGA, with 1393 stores at number one; Bottle O Liquor, with 628 stores in fourth position; IGA Liquor, which has 457 stores at number nine; Thirsty Camel Liquor and Mitre 10, each with 450 outlets at 10; Cellarbrations and its 441 stores at 12; Lucky 7, which has 340 outlets at 20; and Friendly Grocer/Eziway with 303 outlets at 23.

The other Metcash retail brand, Autobarn, sits outside the Top 50, but has 101 stores throughout Australia.

With supply chain re-engineering across the retail industry and direct sourcing by the major chain retailers seriously weakening wholesalers, Metcash has developed a new business model that allows the company to continue as a middle man in the supply chain, but with greater control over its destiny by owning the retail brands under which its customers trade.

While Autobarn was a pureplay before Metcash acquired its established franchise system, Mitre 10 involved the purchase of a retailer owned cooperative that was in debt and losing market share as store numbers and sales declined.

Metcash bought the Mitre 10 retail brand and, as with the supermarket retailers that had previously owned and controlled their own banners, effectively created a franchise system for independent hardware retailers.

The rationale for Metcash moving outside its traditional grocery and liquor business is that it has a core competency in logistics, warehousing, distribution, and retailer support services.

Metcash has annual sales of more than $12.3 billion and earnings before interest and tax of around $450 million. It has succeeded in stabilising market share for the IGA and Mitre 10 retailers.

Food franchises reign

As the retail sector continues to adjust to various challenges, including a tightening in consumer spending, higher costs, and competition from online retailers, retail franchisors are under considerable pressure and scale is becoming an increasingly important factor in maintaining the viability of a franchise system.

In the past three years, store network growth has been flat for most retail franchises systems, with the exceptions being acquisitions such as the Metcash IGA purchase of Franklins supermarkets and 7-Eleven’s acquisition of the Mobil convenience store and fuel network.

In that period, a number of franchises have failed including Souvlaki Hut, Bean Bar, and Pets Paradise, as well as the multi-brand franchisor, Allied Brands, while a number have been acquired by other franchisors as part of a consolidation process that aims to improve the scale of operations in areas such as property management and site selection, IT support, and legal services

Apart from Metcash, there are three major multi-brand franchisors in Australia, all of them in the food business.

Two are in the fast food meals segment, Yum! Restaurants Australia which owns the KFC and Pizza Hut brands, and Quick Service Restaurants which owns the Red Rooster, Oporto, and Chicken Treat chains.

The other major multi-brand player is the publicly listed Retail Food Group which owns Donut King, Michel’s Patisserie, Brumby’s Bakeries, BB’s Café, Esquires, Pizza Capers, Crust Gourmet Pizza, and The Coffee Guy.

Boost Juice has also developed an appetite for other retail brands, acquiring Salsa’s Fresh Mex Grill and, more recently, Cibo Expresso; while Franchised Food Company owns Cold Rock Icecreamery, Nutshack, Mr Whippy,and Pretzel World. Franchise Entertainment Group owns Blockbuster, Video Ezy, and EzyDVD.

The Inside Retail Magazine Top 50 Franchises list is dominated by food and liquor chains with Mitre 10 the highest ranked non-food franchise system with a 450 store network.

Video Ezy is the next biggest non-food retail franchise system with 375 stores and ranked at 15, followed by Priceline Pharmacy at 17 with 360 stores, and Optus World with 295 stores coming in at 25.

A number of Australian born or based franchises have successfully ventured overseas, although some have felt the chill winds of difficult economic conditions in global markets in the past three years.

Among the local franchisors who have built networks overseas are Cartridge World which has stores in 56 countries and is ranked 37th for its Australian retail franchise systems, while Gloria Jeans Coffees has 200 stores in 39 countries. Gloria Jeans is ranked at 13 on the Inside Retail Magazine listings with 428 stores throughout Australia.

Boost Juice, which is places at number 35 with 212 stores in Australia, has also ventured into 14 countries, while Harvey Norman trades in six countries and both Video Ezy and The Coffee Club each have opened stores in five other countries.

Inside Retail Magazine’s Top 50 Franchises includes 23 home grown franchise systems as well as the Australianised Gloria Jean Coffee chain that started in Chicago but was acquired by Australians.

The list also includes the Home Hardware group which is owned by Danks, a wholesaler acquired by Woolworths and Lowe’s as the platform for the launch of the corporate Masters Home Improvement stores.

Woolworths is continuing to supply and support the Home Hardware, Thrifty Link, and Plants Plus banners alongside its burgeoning corporate store network.

Franchise future

The franchise sector continues to be bullish about business prospects and claims that franchise systems continue to outperform other businesses, but retail franchises are still faced with significant challenges as consumer attitudes shift and retailers adapt their business models to offset rising costs and competition from new international players.

Tough economic conditions in the past three years have made some franchisees restless and has increased the number of disputes, but the Australian Competition and Consumer Commission (ACCC) has been criticised for not doing enough in the franchise sector.

The ACCC flagged a more proactive role in enforcing the franchising code of conduct when Rod Sims became chairman in 2011, but there seems to have been limited intervention from the regulator.

The franchising code of conduct itself is currently being reviewed by Alan Wein, one of the founders of the House homewares chain.

This fifth review of the regulations in seven years is examining issues such as good faith in franchising, rights of franchisees at the end of their franchise agreements including recognition for any contribution they have made to building the franchise, and the operation of the Competition and the Consumer Act 2010 with respect to enforcing the code of conduct.

Wein is also reviewing the effectives of amendments made to the code of conduct in 2008 and 2010.

While the Franchising Council of Australia (FCA) is vehemently opposed to including good faith provisions in the code of conduct and the regulatory framework for franchising, support for the concept remains, particularly after inquiries in Western Australia and South Australia.

The good faith concept and the rights of franchisees at the expiry of a franchise agreement triggered both the state inquiries and followed a decision by Yum! Restaurants Australia not to renew franchise agreements for KFC stores in WA operated by Jack Cowin, who also owns the Hungry Jacks chain.

Cowin is understood to be at an advanced stage of negotiations with Yum! for the sale of the 45 KFC stores he still operates under franchise agreements in WA and the NT.

The FCA has welcomed the Wein review, the operation of the Franchising Code of Conduct, and ongoing examination of the regulatory framework for the franchise sector.

Michael Paul, FCA chairman, said the Franchising Code of Conduct continues to provide “a strong and comprehensive regulatory framework that does not impose unreasonable compliance costs”.

Paul says Australia is recognised internationally as having the world’s best franchise regulatory framework.

“The FCA believes some incremental amendments to the Code may be appropriate, but there ought not be any material changes to the framework that has proven to be so effective,” he says.

In November 2012, the FCA in association with the American‐based Institute of Certified Franchise Executives (ICFE), launched the Certified Franchise Executive (CFE) program to its members.

The CFE program is the only internationally recognised professional accreditation program for franchise executives and is known and respected by franchise leaders around the world.

Paul said the program will be used in Australia to ensure the highest professional standards and is a new initiative that augments existing education and training programs developed specifically for the franchise sector.

For retail franchise systems in a highly competitive marketplace, the focus in the year ahead will be on reducing costs, reinforcing brand value and improving standards, particularly in customer service.

The fight to reduce costs is certain to encompass rental and occupancy costs in shopping centres and could see more retail brands reduce their store footprint or co-locate with other compatible brands.

The franchise sector will also be pushing for more flexibility on penalty rates and trying to cap staffing costs and some are likely to exploit the opportunity created by lower interest rates to refinance franchises.

This story originally appeared in Inside Retail Magazine. The August/September issue, featuring exclusive coverage of the 2013 Westfield World Retail Study Tour is available now. For more information, click here.